Why Holding Cash Might Be Riskier Than You Think

Why Cash Feels Safe

Money brings comfort. It’s liquid, liquid, liquid. Cash is not as volatile as stocks or real estate, swinging dramatically from day to day, and so many people see cash as the safest financial position on an instinctive basis.

But safety depends on how you define risk.

If risk only means volatility, then cash appears secure. However, if risk includes the gradual loss of purchasing power, cash becomes far more vulnerable than many people realize.

This is one of the most misunderstood realities in personal finance: money can look stable while slowly losing value over time.

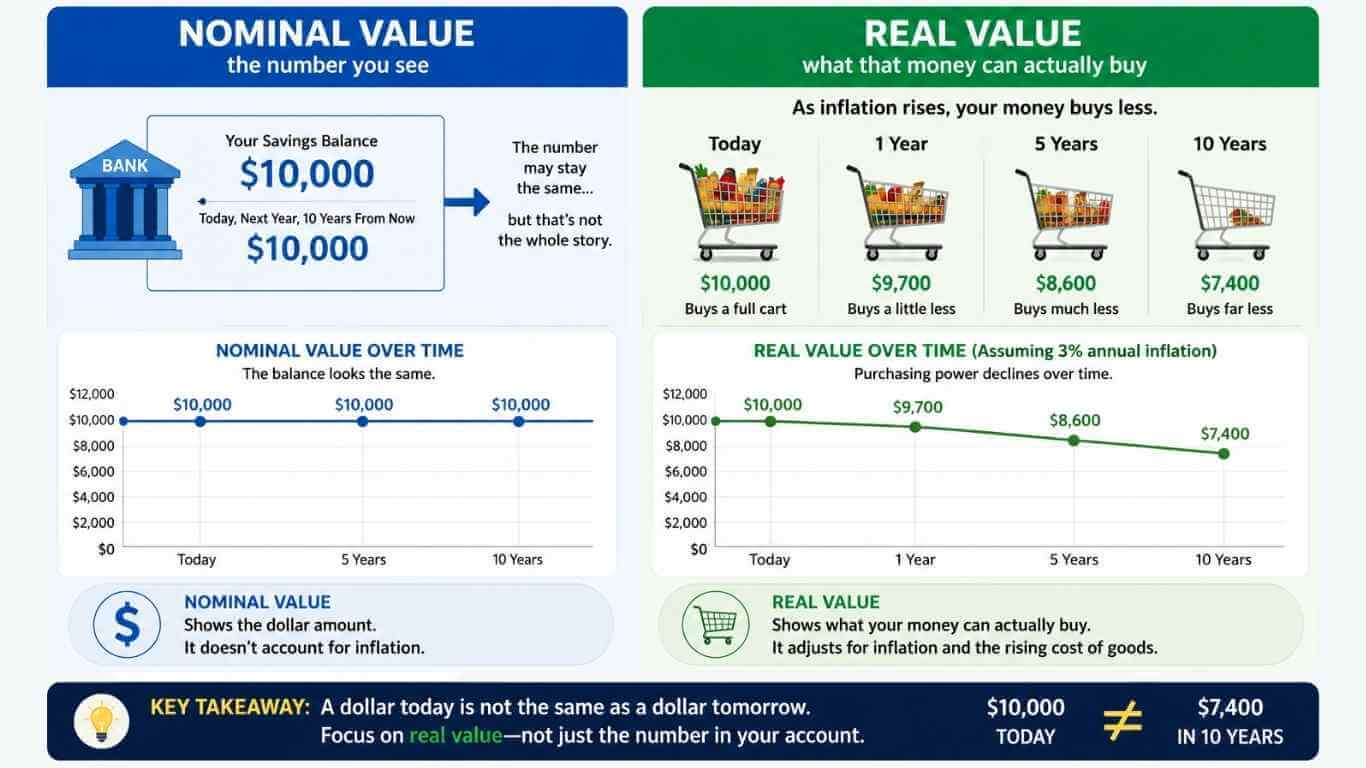

The Difference Between Nominal and Real Value

One of the most important financial concepts is the difference between:

- Nominal value → the number you see

- Real value → what that money can actually buy

For example:

- If your savings account pays 1% interest

- But inflation is running at 3%

- Your actual purchasing power is declining at about 2% per year

Even if your account balance goes up a little bit, the value of that money goes backwards in practical terms.

This concept connects directly to what was discussed in Why Inflation Quietly Destroys Your Purchasing Power: inflation compounds over time, quietly reducing what money can buy.

Why Inflation Changes the Meaning of “Safe”

Inflation fundamentally changes how people should think about cash.

A dollar today does not necessarily hold the same value years from now. According to the U.S. Bureau of Labor Statistics (BLS), the purchasing power of the dollar has steadily declined over decades due to inflation.

This means:

- Savings may not go as far in the future

- Fixed income erodes over time

- Everyday expenses are more difficult to absorb

The problem is not just inflation spikes, it’s sustained inflation over long periods.

As explored in How Inflation Quietly Taxes Your Money, inflation functions like a hidden cost that steadily reduces purchasing power without appearing directly on a statement or bill.

Why Cash Might Get More Vulnerable Over Time

You need to have some cash available for liquidity and emergency needs. The problem is large sums sitting idle for long periods of time, not keeping pace with inflation.

Over time:

- Housing costs are rising

- Your insurance premiums are going up

- Groceries become more expensive

- Healthcare and education costs rising

If savings growth lags behind those increases, the gap compounds.

That’s why long-term purchasing power matters more than holding on to a static dollar amount.

The Difference of Ownership

One of the reasons why investors like Warren Buffett tend to talk more about owning things versus owning cash, is that productive assets can change over time.

Assets such as:

- Businesses

- Real estate

- Equities

can generate income and potentially grow alongside inflation.

Cash, however, is fixed in nominal terms unless it earns a sufficient return.

This doesn’t mean all investments are guaranteed to work out or be free from volatility. But historically, having something has been a better long-term hedge against inflation than just sitting in cash on the sidelines.

Why People Still Hold Too Much Cash

Even with inflation, many people keep large amounts of cash on hand, because:

- It feels safe emotionally

- Market volatility causes fear

- Economic uncertainty encourages caution

These reactions are understandable.

But sometimes an emphasis on short-term stability can mask long-term erosion. Inflation is a slow-working thing, and the effect is easy to miss in the moment.

This ties back to the broader discussion introduced in The Truth About Money Most People Aren’t Told: money is constantly influenced by forces that operate quietly over time.

Why This Matters More Today

In a context where:

- Inflation remains high compared to historical targets

- Interest rates differ

- With living costs continuing to rise,

understanding purchasing power is becoming more and more important.

It’s not just about saving money anymore. It’s saving what money can do.

The Bottom Line

Cash may feel safe because its dollar amount stays stable. But stability and purchasing power are not the same thing.

When inflation consistently outpaces the return on savings, the real value of cash declines over time.

Understanding this difference is essential for anyone trying to think long term about money, savings, and financial security.